What’s the Score?

What’s the Score?

Credit scores are usually a three digit number. What does the number mean? How do I successfully interpret and use it? That’s the issue where most lenders can begin to fail or take the wrong path because Credit scores do not predict whether a borrower will repay or default on a loan.

Credit scores do not identify “good” or “bad” applications on an individual basis. Both paying and nonpaying loans often have the same score so it is the task of the lending organization to attempt to distinguish which loan will pay and which will not. To further complicate the process each credit score used will result in a different score for the same applicant.

The major credit reporting agencies Experian, Equifax and Trans Union provided data from their subscribers and a credit score model was developed for each CRA. Since the data provided was different for each CRA the models did not result in the same score.

Let’s start by reviewing the credit score you are using today.

Types of Credit Scores

Credit scores can be divided into three classes – custom scores, generic scores and hybrid scores. The most important difference in the types of scores is found in the makeup of the data used to formulate the model.

Custom scores are the most accurate measure of creditworthiness because they take into consideration information specific to the applicant based on data from the credit grantor’s previous loans. Custom scores utilize traditional aspects of the applicant’s profile to evaluate risk including time employed, length of residence, home ownership and debt ratio as well as the applicant’s payment history that is a major factor in every generic score reported by the credit bureau.

Custom scores collect data against the record of paying and nonpaying applicants from the past experience of the lenders own history to provide the basis to measure future credit risk. Because of the specific population being studied, a custom score is more predictive and precise in determining the applicant’s probability of repayment.

Generic scores like the FICO, Vantage or BEACON scores are based primarily on borrower repayment experience reported by credit reporting agency subscribers and are intended to be applied over a wide geographic and demographic group of applicants. Reported repayment history and utilization of credit is the basis for the score.

The Hybrid Credit Score Option

Both custom and generic credit scores have serious limitations. Custom scores require large amounts of data that may be difficult to obtain, expensive integration with loan origination systems and sophisticated algorithms developed by statistical analysis.

Generic credit scores can only produce general estimates of probable repayment because 65% of the score is based on two lending consideration, the applicant’s total amount owed and prior repayment history.

Generic scores will seldom result in an accurate measure of individual applicant creditworthiness because they do not include the traditional elements necessary to evaluate credit risk such as debt to income ratios, home ownership and applicant employment or residence stability.

Our experience supports the use of a third option, a hybrid credit score, as the best tool available for consumer lending. A hybrid score combines select custom application data from your own paying and nonpaying loans to enhance the accuracy of the widely used generic scores. The hybrid credit score option allows the lender to benefit from the accuracy inherent in the traditional custom score variables and use the generic score to competitively price all products.

Using Multiple Credit Scores

I’ve encountered lending managers who have been so dependent on credit scores that they decide to use two or even more scores simultaneously. The adoption of multiple credit scores to qualify applicants for specific loan products presents challenges that may result in unintended issues. Because each credit score has different minimum and maximum ranges, an applicant’s score reported from each scoring model will not be a constant. Depending on the model and score used an applicant could have their credit score vary by 50 or more points, placing the decision to approve/decline and pricing into a different risk category.

Variance of Credit Scores

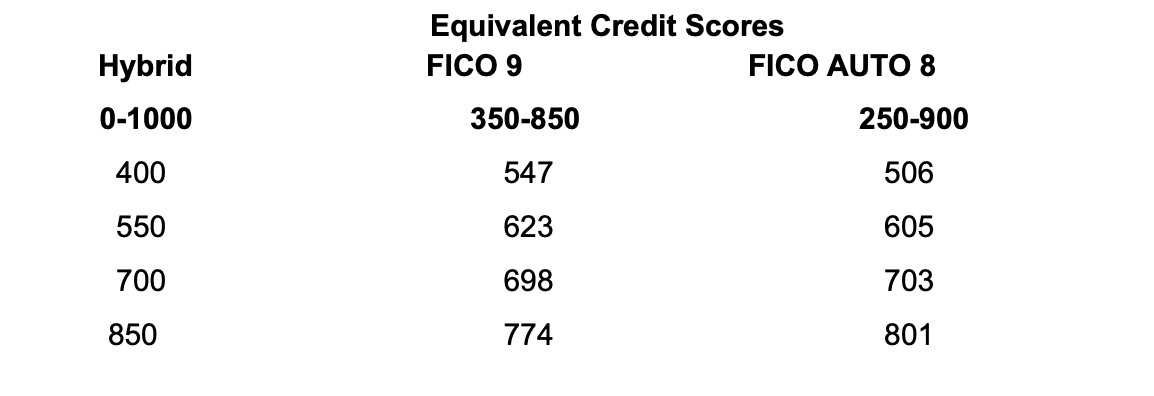

The chart below compares the equivalent credit score for an applicant based on several generic scores widely used today. The comparison is based on the difference in each model’s designed scale. A hybrid score has a scale from 0 to 1000, FICO 9 from 350-850 and the Auto FICO 8 from 250-900.

Applicants with lower scores will see the greatest variance. This is crucial near the risk and/or pricing cut off margins for each score. Understanding the scoring model objective is essential. Generic scores such as FICO or BEACON are not intended to determine whether an individual applicant will repay, but to estimate the percentage of applicants in a score range that are expected to be 90 days past due in one year. Every lending and financing entity should closely monitor the effect of using multiple credit scores to fund loans. Using multiple scores based on variables, weights and scales that are unalike increases the difficulty in applying the scores without issues of possible discrimination.

Applying hybrid scores to enhance generic scores resolves many issues. The custom variables obtained from your own applications will improve predictability because they represent values that are specific to your demographics and previous data used to make decisions. The generic score element will allow flexibility to include competitive pricing options developed for lending to a diverse and non-parametric population.

To obtain an estimate and proposal for converting your current credit score lending program to a Hybrid scoring system contact sales@creditscorelending.com.